A vast majority of people get to choose which pension or retirement fund they want their payments to go into. You can always choose to stick with the fund you already have, use the fund your employer gives you, or even choose a different fund.

Table of Contents

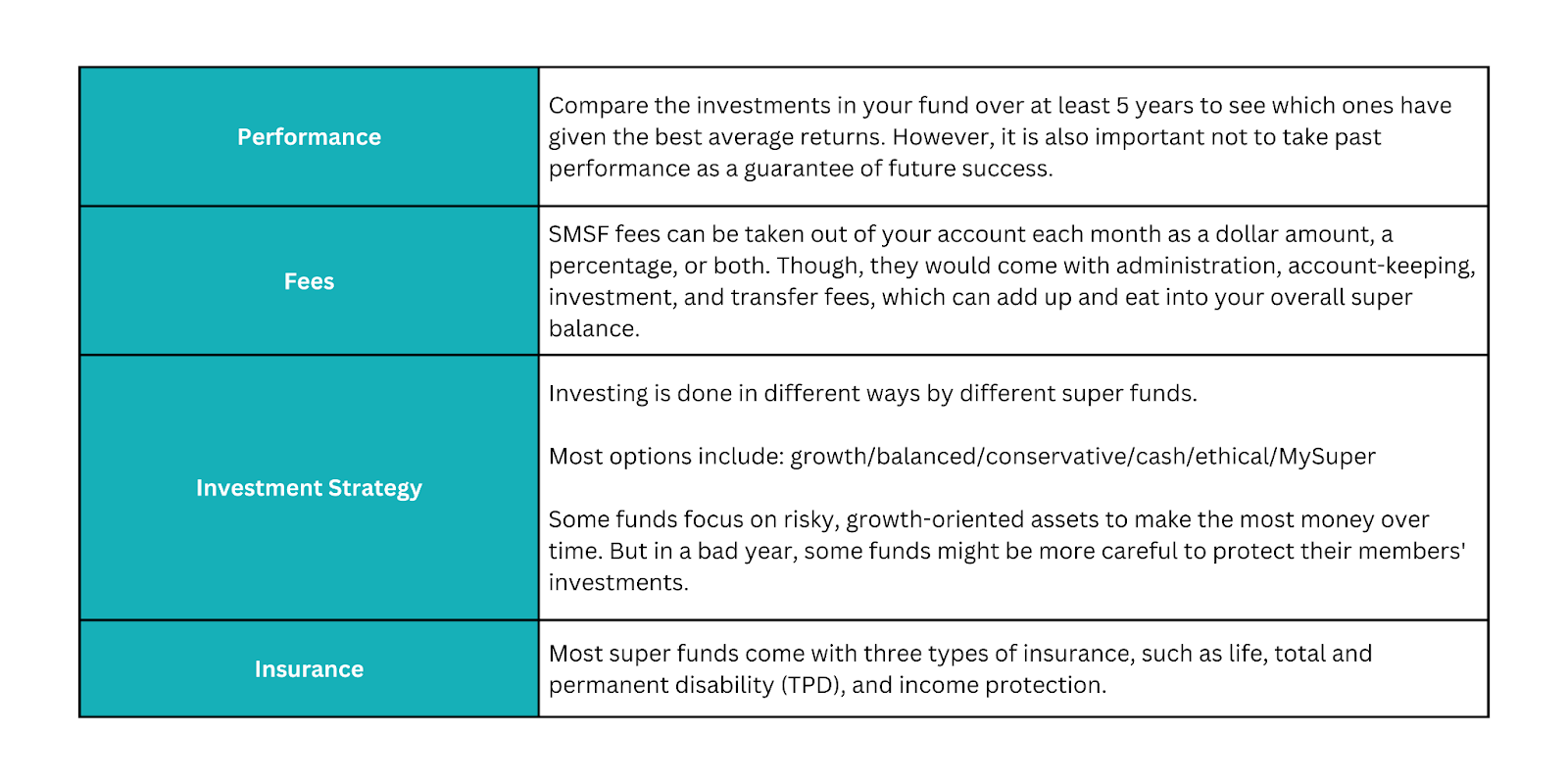

Here are some things you should look out for in a super fund:

If all of this is still too much for you to handle, don’t worry. The ATO has a comparison tool that will help you compare your MySuper products and choose what’s best suited to your financial situation or lifestyle.

Is there insurance on inactive superannuation fund?

In accordance with Australian law, super funds are required to cancel insurance on low-balanced inactive super accounts that haven’t received contributions for at least 16 months. Fret not, as you will be contacted if your insurance is about to end.

When this happens, you can keep your insurance, but you have to do one of the following: tell your super fund; OR

contribute the remaining amounts to an existing super account.

If you join a super fund for the first time and are under 25 or have less than $6,000 in your account, your superannuation fund won’t offer insurance for you.

When this occurs, you’ll need to contact your fund to ask for insurance through your super, unless you’re working in a dangerous job and your fund decides to automatically cover you.

But if you already have insurance in place and your balance is less than $6,000, you won’t risk losing it.

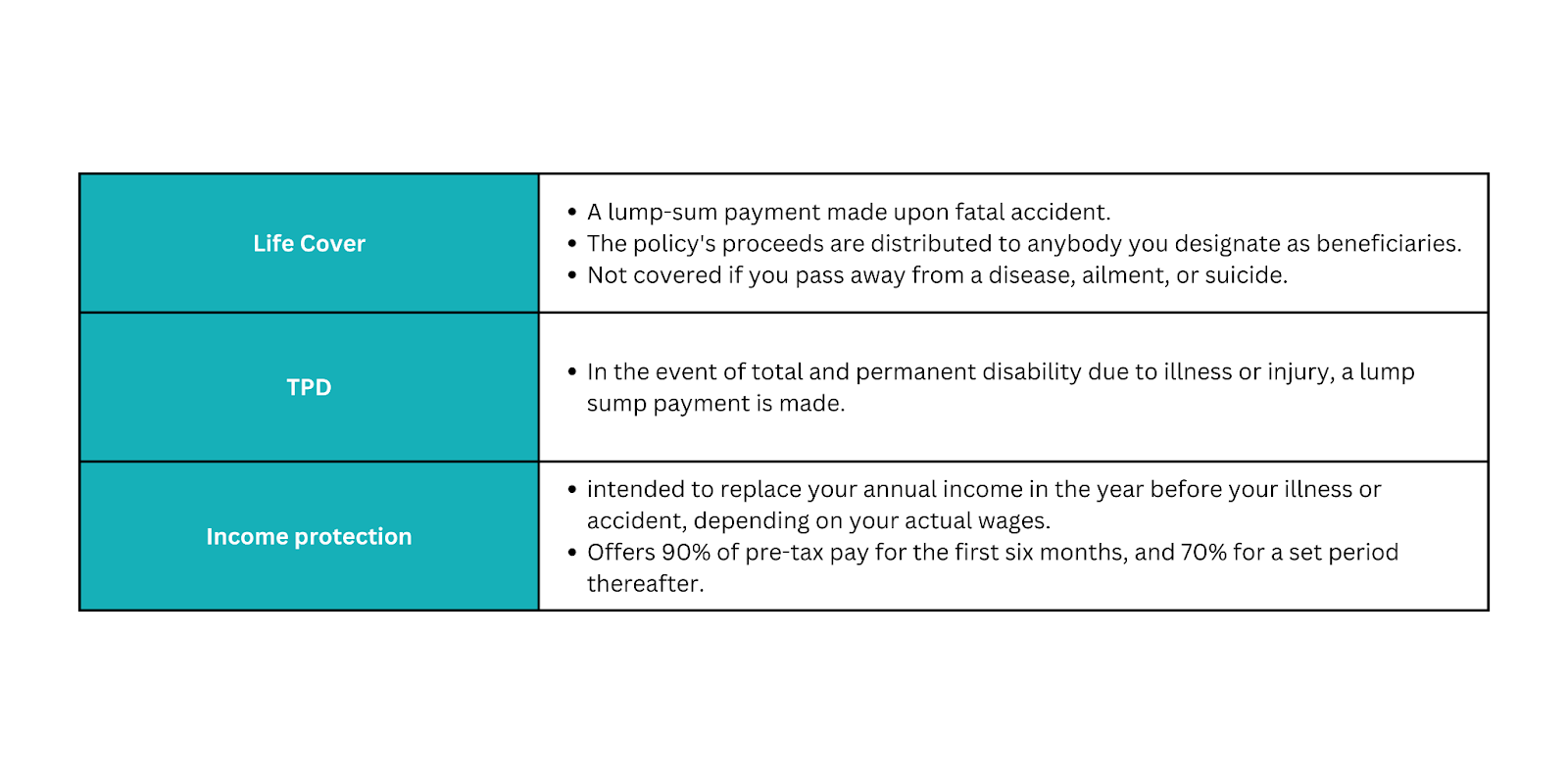

What available insurance is there?

Pros & Cons of Insurance through Super

Pros:

- It’s easy to pay because it’s taken out of your super account automatically.

- easy to increase amount of cover

- Tax-effective as only 15% tax payment are required

Cons:

- Coverage is limited as it’s less than what you can get from insurance outside of super.

- Coverage can end when you switch super funds or your account becomes inactive.

- Lower super balance because money is taken out to pay for insurance.

Who should I contact to claim my insurance & how?

Who you should talk to about the insurance policy depends only on where you bought it.

This could be:

- an insurer, if so, contact the insurance company;

- an insurance broker or financial adviser;

- a superannuation fund; OR

- an employment arrangement

Get in touch with them and provide any supporting paperwork, like medical records, payslips and tax return, a death certificate that they may require to process your insurance claim.

The claim process will depend on the circumstance but should take approximately 2 to 6 months. To gain a clearer picture of processing time click here.

We’re here to help

At Mint Super Audit, we place a significant emphasis on attending to the requirements of our clients and delivering SMSF services that are of the highest possible quality.

Just clicking on this link will take you to further information about our company. Also, we offer seamless online smsf audit services for SMSF audits through this website.